EQ Bank: First Home Savings Account

Designed a post-onboarding funding widget that appeared at the peak moment of user intent — driving a 30% increase in initial funding conversions and reaching 150% of our annual deposit target in just 6 months.

EQ Bank, a Schedule I digital bank in Canada, launched in 2016 and has since amassed over $9 billion in deposits, serving more than 500,000 customers as of OCT 2024. Recognized as Canada's leading bank, EQ Bank secured the #1 position on Forbes' World's Best Banks list in 2024, a title it has held since 2021.

Role, responsibilities, project duration

As senior product designer at EQ Bank I led the end-to-end design for FHSA, working with a core team of five across various business units. We were able to successfully delivered this product from concept to production in just 3 months.

I introduced a key innovation: the first-time funding feature in the account opening flow. This feature allowed immediate saving (after they open the product), aligning with customers' home ownership goals and significantly contributing to the product's rapid adoption and business growth (30% total deposit).

Business goal

The First Home Savings Account (FHSA) is a groundbreaking registered account introduced by the Canadian government to empower first-time homebuyers. Similar to TFSAs and RRSPs, it offers unique tax advantages, allowing tax-free growth and tax-deductible contributions. With an annual contribution limit of $8,000 and a lifetime maximum of $40,000, the FHSA provides a powerful savings tool for aspiring homeowners.

Since its announcement in early 2023, the FHSA has generated significant buzz across online forums and social media platforms. Recognizing the immense potential and high demand for this innovative financial product, as a top business priority, EQ Bank’s goal is to be first-to-market with this new financial product in order to capture customer demand.

Research insights

The First Home Savings Account (FHSA), being a new product, posed challenges in predicting customer behavior and expectations. To address this, we conducted extensive research to understand how FHSA could help customers overcome obstacles in saving for their first home.

Our research team interviewed existing and potential customers, gathering insights on home-saving strategies, challenges, and FHSA expectations. These findings were instrumental in shaping our approach. Key discoveries include:

User problem

Based on the research from interviews and surveys, I defined user problem based on three categories

Actions: specific behaviours that users do today to save

Feelings: heightened emotion users feel when they think about purchasing or start saving for their first homes

Needs: things or experience that users need to feel motivated to use FHSA in their life

Drawing from our research insights, I crafted these three key design goals for FHSA.

Customer journey

To address these design goals, I began by developing a comprehensive customer journey map. This map outlines the customer's mindset, actions, and emotions throughout the FHSA experience. We identified 5 key phases in the customer journey:

Awareness: Discovering and learning about the FHSA

Onboarding: Opening and setting up the FHSA

Funding: Initiating one-time and recurring deposits

Management: Tracking progress and optimizing contributions

Utilization: Maximizing contributions and planning for withdrawal

By analyzing customer intentions and mindset at each phase, I identify key moments and opportunities in the journey. This allows me to design an optimal path that guides users towards their goals efficiently and intuitively. The focus is on delivering the right information at the right time, creating a seamless experience that boosts confidence in decision-making and minimizes anxiety. This approach ensures that users can navigate the FHSA process with ease, from initial awareness to final utilization.

Wireframes

Some of the intial thinking focus on introducing a personalized plan that’ll help customer save and reach their financial goal towards their first home. Key experience include;

Detailed questionnaire; to help customer plan their goal and understand their situation

Visual calculator that projects future earnings; to provide choices and help customer make a decision

First time funding and automated saving; to help customer to act on that plan with one-time setup

Modular dashboard with goal setting and education; to remind customers of their progress & what to do next

The concept was initially explored for web first because 75% of the EQ customers open products through web browser. Unfortunately, I didn’t have a chance to explore mobile before we made the cut off on these features.

Design

Despite numerous opportunities for exploration and iteration, we faced a tight timeline and technical constraints in order be first-to-market. This necessitated intentional design choices focused on delivering core value. Our key priorities were to ensure customers could:

Easily understand the product and how it’s different from TFSA & RSP

Open an account quickly and securely

Fund their account seamlessly to start contributing and earning immediately

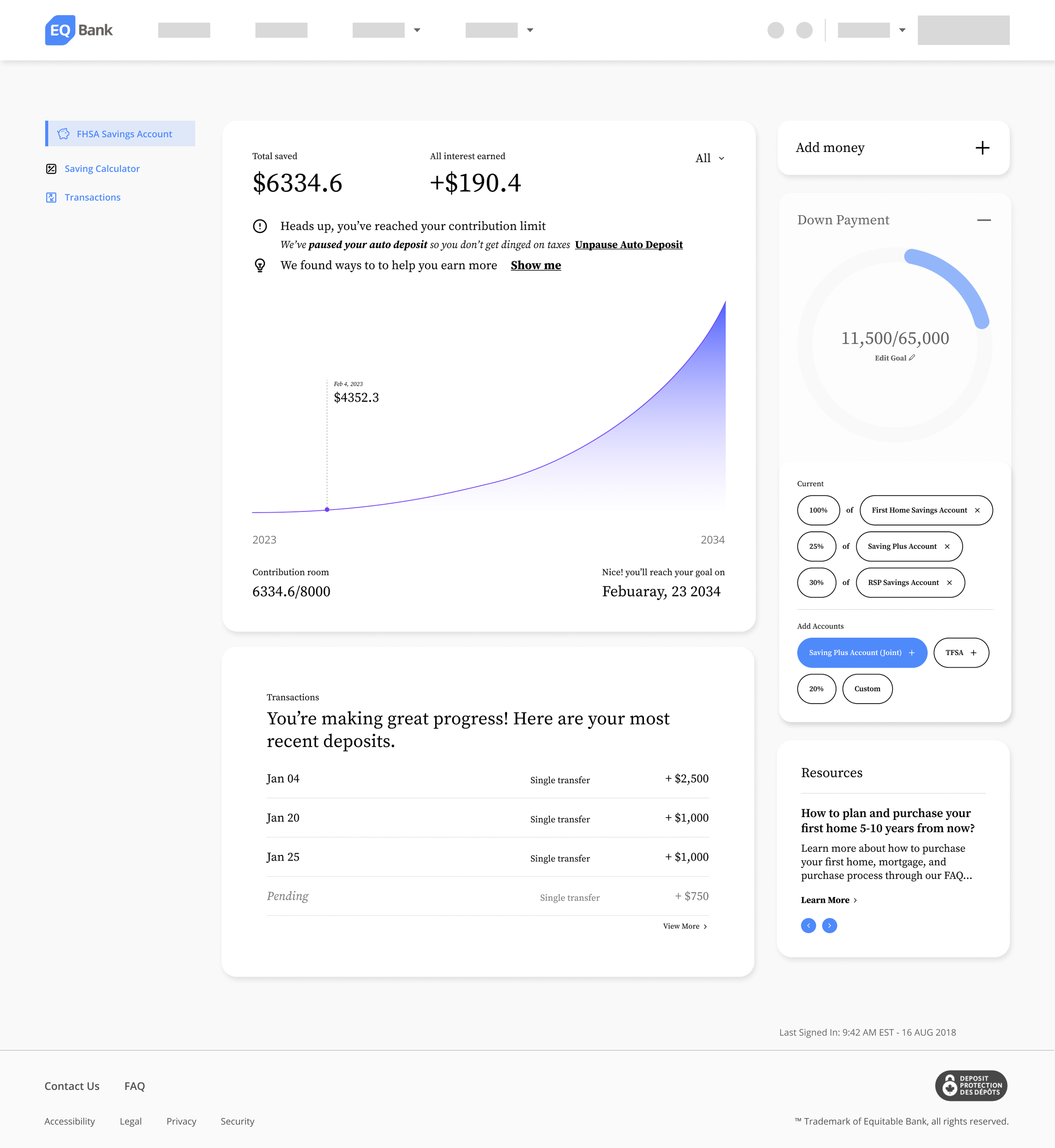

To achieve a lean design solution within our constraints of limited resources and a tight deadline, we strategically introduced a first-time funding feature during the account opening process. This approach allowed us to maximize value delivery while maintaining efficiency in our development timeline.

Our initial design concepts explored a comprehensive guided path to address all the challenges identified in our research, including personalized questionnaires, projected earnings calculations, streamlined account opening, and funding processes. However, due to resource constraints and tight deadlines, we had to adopt an MVP (Minimum Viable Product) approach.

To prioritize key experiences and features, we employed the MoSCoW prioritization framework. This analysis revealed that enabling funding during the onboarding flow was a core customer need, leading to the development of our first-time funding feature.

The strategic placement of this feature in the account opening flow was based on two key psychological principles:

1. Peak-End Rule

We positioned the funding widget on the success page, capitalizing on a key moment in the customer journey. The peak-end rule suggests that users most vividly remember the peak and end of an experience. By placing our funding option at this crucial endpoint, we ensured maximum visibility and engagement.

2. Principle of Least Effort

While customers' immediate goal is to complete the account opening process, their underlying need is to save and earn for their first home. By offering the funding option immediately after account creation, we aligned with the customers' true intentions and provided a convenient, low-effort path to fulfill their savings goals. This approach leverages the natural human tendency to choose the path of least resistance, increasing the likelihood of immediate account funding.

In addition to the first-time funding widget, we implemented targeted UI and content updates throughout the product experience. Despite our resource limitations, these enhancements significantly improved the overall user experience, representing a substantial achievement given our constraints.

Customer can open account within seconds and fund right away after account is opened, which help kickstart their saving & earnings and gets them closer to their goal.

Impact

The First Home Savings Account (FHSA) has surpassed expectations, establishing new standards in product development efficiency and deposit accumulation:

Swift Launch: Developed and released in just 3 months (July 19, 2023)

Remarkable Growth: Reached 52% of annual target within 3.5 months, escalating to 148% in 5.5 months (December 2023)

First-Time Funding Triumph: 30% of total deposits attributed to new feature, with 46% customer adoption rate

Steady Expansion: Maintained 30% month-over-month increase in account sign-ups

Financial Impact: FHSA contributed a significant ~18% to Q4 earnings, demonstrating its pivotal role in EQ Bank's portfolio. For comprehensive details, refer to the FY2023 annual earnings report.

EQB surpassed raised earnings guidance for ten-month FY23 with strong revenue

Adjusted and reported Q4 revenue1 $395 million and FY23 $944 million (reported $976 million) on lending growth, NIM expansion and higher non-interest revenue

EQ Bank customers +30% in FY23 to over 400,000 with deposits of $8.2 billion

EQ Bank customer base +9% q/q and +30% y/y as daily account openings accelerated in 2023 due to the increasing popularity of the Savings Plus Account that operates like a high interest chequing account, as well as the addition of new digital offerings such as the EQ Bank First Home Savings Account (FHSA), the introduction of the EQ Bank Card and expanded offerings in Québec

The FHSA's impressive performance - reaching 150% of our annual target in just 6 months - demonstrates the power of aligning product development with genuine market needs. This success has significantly contributed to EQ Bank's overall growth, accounting for approximately 18% of Q4 earnings.